A Look at 2026 Big Tech Shareholder Proposals

Tech giants continue to face proposals on wide range of topics, including how AI intersects with broader questions of accountability, transparency, and risk management.

The Foundation Matters More Than the Model

Why Trusted Data and Human-Centric AI Will Define the Next Era of Investment Stewardship

What the SEC’s Semiannual Reporting Rule Means for Governance

A review of the debate landscape surrounding semiannual reporting and its governance and stewardship implications.

New From Glass Lewis

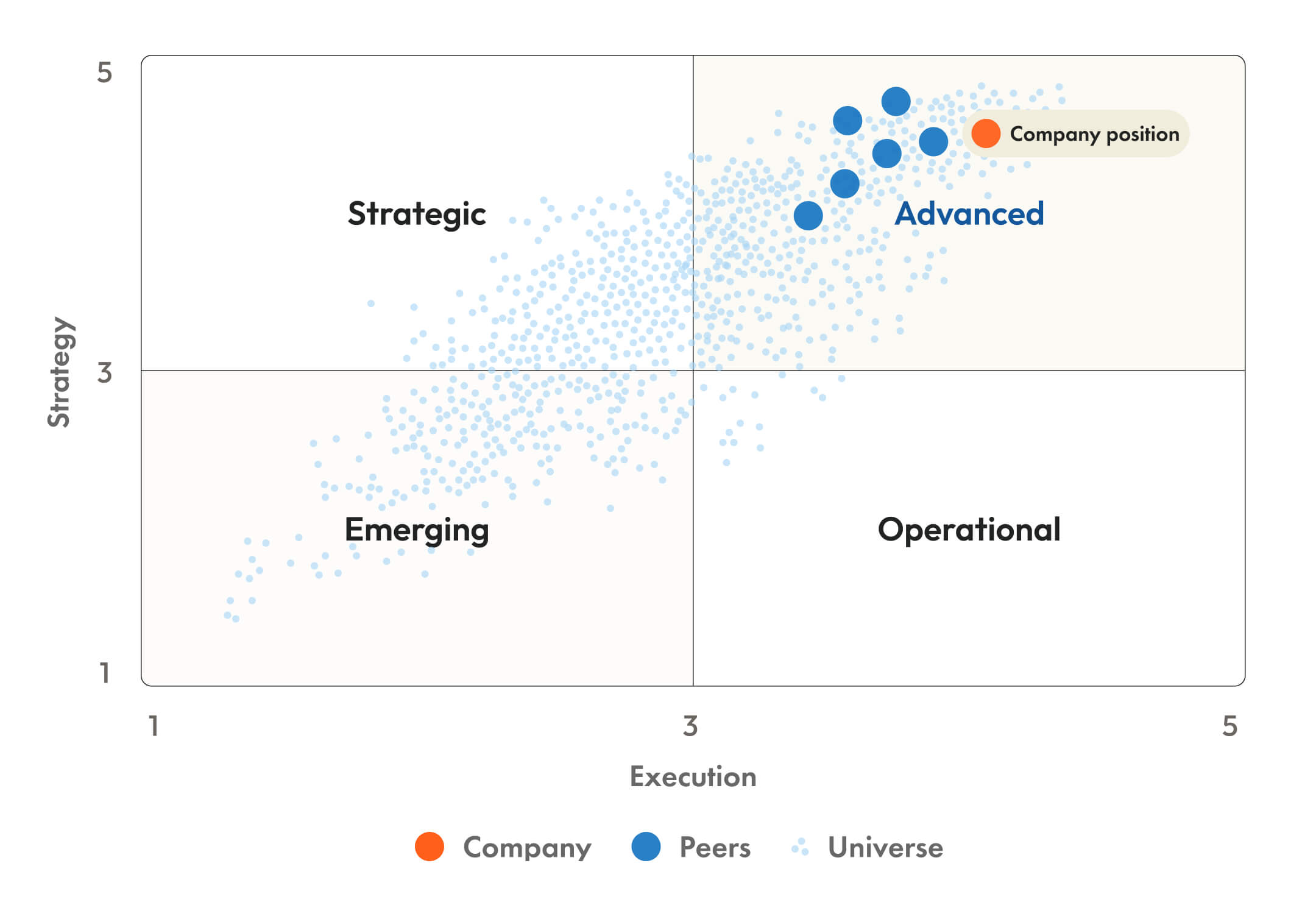

Next Generation Climate Research for Investors

Forward-looking, financially material insights on how companies are managing their transition risks and opportunities.

Governance and Voting Solutions for Smarter Decisions and Seamless Workflows.

Corporate Governance Solutions to Advance Governance-Related Strategies.

A Look at 2026 Big Tech Shareholder Proposals

A Look at 2026 Big Tech Shareholder Proposals

A Guide to the 2026 PRI Reporting Framework: Mapping Indicators to Glass Lewis Services

A Guide to the 2026 PRI Reporting Framework: Mapping Indicators to Glass Lewis Services

Where Stewardship is Heading: Survey Findings on Outsourcing and Oversight

Where Stewardship is Heading: Survey Findings on Outsourcing and Oversight

Podcast | Activist Investing Today: Glass Lewis' Timmer on AI, Future of Governance

Podcast | Activist Investing Today: Glass Lewis' Timmer on AI, Future of Governance

Why Choose Glass Lewis?

Founded in 2003, Glass Lewis operates globally with offices in North America, Europe, and Asia Pacific, including locations in San Francisco, Toronto, London, Limerick, Karlsruhe, Paris, Sydney and Tokyo. Our innovative solutions support governance and stewardship efforts worldwide.

Learn how Glass Lewis supports corporate governance and stewardship best practices.

Book an initial conversation.

Next Generation Climate Research for Institutional Investors

Forward-looking, financially material insights on how companies are managing their transition risks and opportunities.

Glass Lewis Climate Intelligence helps investors evaluate how companies’ transition strategy and execution drive long-term value.