Shareholder activism is on the rise. As a result, some have reasonably asked whether proxy advisors like Glass Lewis are helping to fuel the surge by more frequently supporting dissident campaigns.

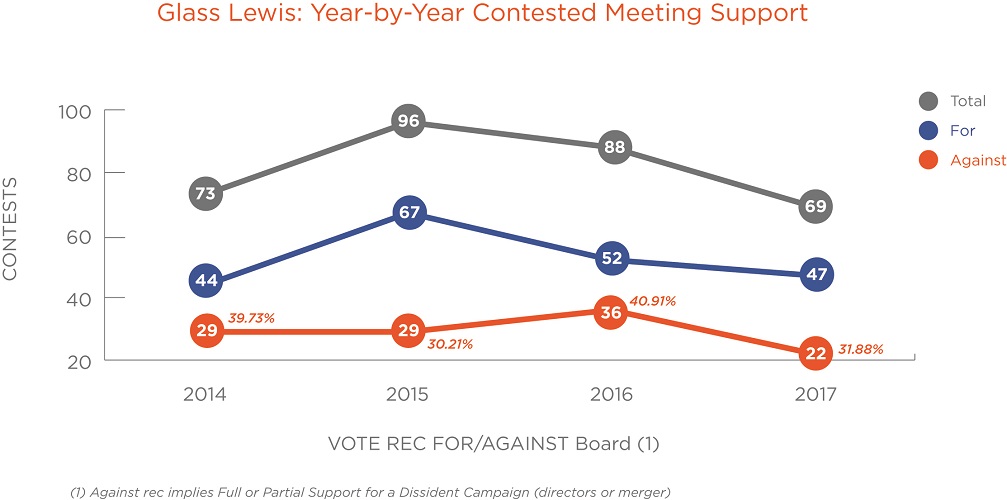

This perception isn’t borne out by the overall numbers. We’d caution against reading too much into the data, since the yearly sample of contested meetings is both too small to be free of significant variance, and too big to reflect the particular combination of parties and moving parts that makes each contest unique. That said, Glass Lewis’ support for contests dropped from 40% in 2016 to 32% in 2017, and has historically stayed within that range. Nor has Glass Lewis’ approach to contested meetings changed in a way that would result in increased activist support; our methodologies, our case-by-case approach and our team have remained consistent.

What has changed is the activist landscape. More and more investors are entering the activist space, including more first-timers running full solicitations. Despite this, the number of contests covered by Glass Lewis is actually down, potentially given boards’ willingness to engage with activists before a full contest breaks out. In cases like Meg Whitman at HP, boards appear to be looking at the potential appointment of activist representatives in terms of adding value, rather than simply avoiding strife.

When matters do develop into a full contest, some larger activists are developing more robust campaigns, in certain cases presenting fully developed alternative operational plans for shareholders to consider. There is a broader shift of activists moving away from strong-arming short-term changes, such as cash dividends and real estate sales, and toward the pursuit of meaningful operational changes coupled with long-term shareholder involvement. These activists have been portrayed as ‘taking a page out of the Private Equity handbook’ in their approach and focus on effecting substantial operating or strategy changes.

This combination of long-term goals, sophisticated tactics and significant investment has allowed activists to pursue larger, more established companies that perhaps were not previously at risk of a shareholder campaign. As well known companies are targeted, the contests themselves are generating more headlines; and with campaign strategies getting more and more refined, Glass Lewis supported some, but not all, of the highest profile dissidents in 2017 — for example at Arconic, Cypress Semiconductor and P&G. There were also a number of large contests where we supported management (General Motors, Buffalo Wild Wings and Ardent Leisure), and as noted above Glass Lewis’ overall support for 2017 contests was at the lower end of the historical range; nonetheless, the combination of high profile contests, and sophisticated campaigns, may explain a perception of increased overall dissident support.

Jason is Senior Director of M&A Research, leading the team that covers all mergers and contested meetings.