Glass Lewis’ two-pronged approach to executive compensation analysis in the North American market is delineated between the quantitative analysis and a qualitative assessment. The quantitative portion, while anchored by the pay for performance grade, incorporates additional considerations to supplement the standardized pay for performance analysis.

CGLytics’ suite of tools is fast becoming an integral part of the quantitative analysis for the North American market. In July 2019, the Compensation Analysis section became a part of Glass Lewis’ Proxy Paper for S&P 1500 companies in the U.S. and Canada. The page illustrates total realized compensation of CEOs based on data provided by CGLytics. Covering the past three years, realized CEO pay is presented on both an absolute basis and relative to country and industry peer groups developed by Glass Lewis using CGLytics tools.![]()

In the following discussion, we examine the aforementioned “additional considerations” regarding the quantitative examination with respect to Capri Holdings, Inc. (formerly Michael Kors Holdings Ltd.) using CGLytics’ analytical tools.

Review of Capri Holdings’ Compensation Program

On August 1, shareholders gave their appraisals of executive pay practices at Capri Holdings, casting votes in favor or against the compensation packages of its named executive officers. The company is one of the few in the broader markets where multiple named executive officers receive pay at the CEO level or higher. Michael Kors as chief creative officer (CCO) and honorary chair and John Idol as CEO have received largely equivalent pay packages for most if not all of Capri Holdings’ history as a publicly traded company.

Multiple CEO-level pay recipients at individual companies have drawn the ire of shareholders in the past and no doubt will continue to do so in the future. However, executives from the apparel industry who engaged with Glass Lewis note that the industry is distinct in that the parity between chief executive and chief creative officer pay is not uncommon, but CCO pay is rarely reported on the Summary Compensation Table as these officers are not typically considered executives. In Capri Holdings’ case, however, perhaps because of his additional title of honorary chair, Mr. Kors is thus a named executive officer whose pay is subject to scrutiny at the Company’s annual advisory say on pay vote.

Overview of the Pay For Performance Grade and the Compensation Analysis Page:

Despite its dual CEO pay level executives, Capri Holdings received a “C” grade under Glass Lewis’ pay for performance model in each year from fiscal years 2015 to 2018, indicating adequate alignment. But in fiscal 2019, the company received a “D” grade after a jump in equity compensation to Messrs. Kors and Idol pushed Capri Holdings’ three-year weighted average compensation levels up – a move unsupported by the company’s weighted average performance that dipped in this year’s analysis. The analysis concluded that the company paid moderately more than its peers but performed moderately worse compared to peers.

Unique situations such as Capri Holdings’ case demonstrate the benefits that additional quantitative analyses have had in Glass Lewis’ approach to executive compensation. One might contend that the pay for performance grade penalized Capri Holdings for common industry pay practices of chief creative officer pay, boosting total named executive officer pay above peers that do not also list their chief creative officer as a top executive.

The CGLytics-powered Compensation Analysis page in Glass Lewis’ research provided additional perspective to help consider Capri Holdings’ executive pay situation. Its focus on CEO pay underscored concerns flagged by the pay for performance analysis. In the same year that the company granted $7.5 million in equity incentives to each of Messrs. Kors and Idol, Mr. Idol’s fiscal 2019 total realized pay increased by 210% from $22.2 million to $68.9 million. At the same time, the Compensation Analysis reported that the median CEO total realized pay among industry peers remained relatively stagnant, highlighting the stark difference in realized pay levels for the CEO position at Capri Holdings compared to peers. While many companies often cite retention concerns due to low realized or realizable pay as reasons for significant increases in equity grants, the analysis using CGLytics indicated this to not be the case, at least for realized pay to the CEO.

Additional Perspectives Through CGLytics:

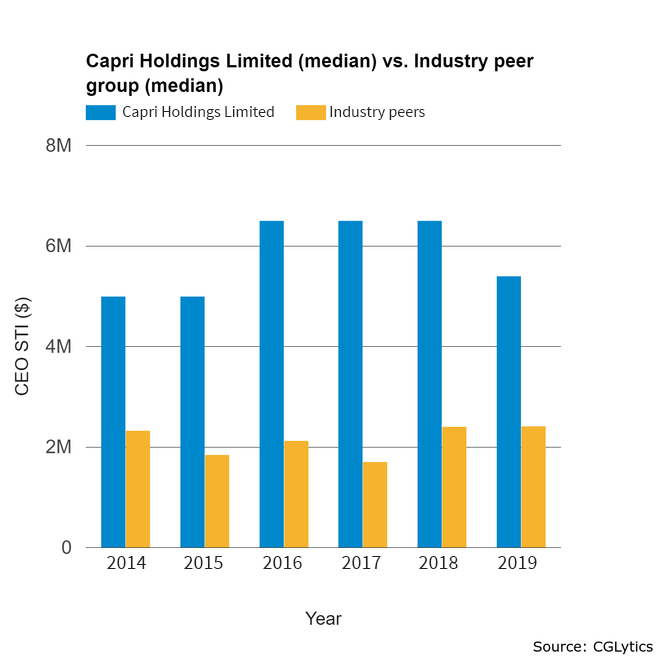

Beyond the Compensation Analysis page, by focusing on CEO pay using the CGLytics’ broader suite of tools, Glass Lewis found evidence to suggest deeper concerns with pay-setting for the short-term incentive. While the company provided Mr. Idol with no LTIP award in 2018 and only $1 million in 2017, the company’s incentives focused on short-term performance made up for the deficiency. Using CGLytics we can observe the following short-term incentive payout comparison to the industry peer median for most of Capri Holdings’ history as a publicly traded company where 2018 represents the most recently completed fiscal year for the company:

In our view, excessive upside opportunities under a bonus plan may unduly incentivize short-term performance and may undermine a long-term focus on company performance among executives. In fact, Mr. Idol received his maximum payout opportunity under the short-term incentive every year since 2012.

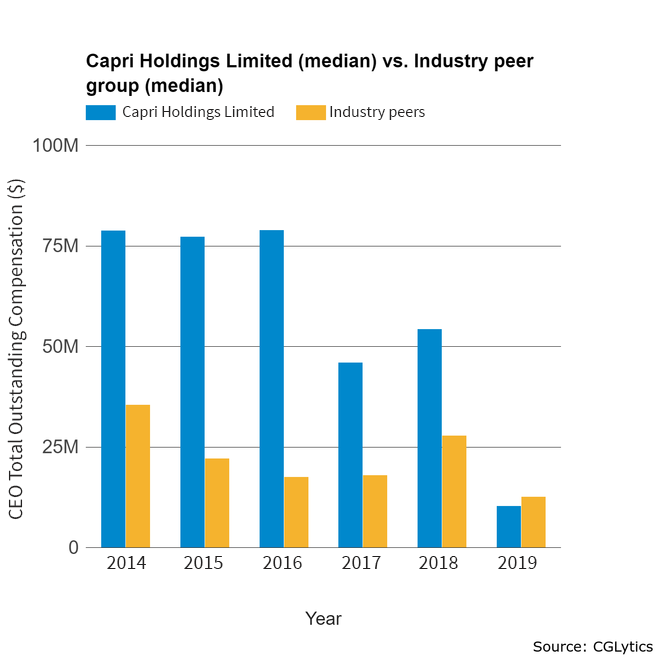

Switching gears in 2019, the Company decided to grant Mr. Idol $7.5 million in long-term incentives. Indeed, the grant resuscitated the level of Mr. Idol’s outstanding compensation following the exercise of a significant number of stock options. Mr. Idol exercised options to acquire 906,076 shares in fiscal 2019 – a value of $58.3 million according to the company’s proxy statement. The following chart shows the change in Mr. Idol’s total outstanding awards with the 2018 data representing the company’s fiscal 2019 and showing the net effect of his exercise of options and increased levels of long-term incentive grants during that year:

The effects of the long-term grant on total CEO pay was quite pronounced as seen in the graph below:

Review of GL recommendation:

In the end, an 89% year-over-year jump in Mr. Idol’s pay placed it at the 85th percentile of CEO compensation compared to the company’s self-disclosed peer group. The pay decisions for fiscal 2019 degraded the alignment between pay and performance in our analysis. Additional analysis into the quantum of pay for Mr. Idol through CGLytics compounded our concerns. That Mr. Kors’ pay presented similar issues as Mr. Idol’s was also considered.

A deeper dive beyond our initial pay for performance analysis into the CEO’s total direct compensation uncovered a history of over-focus on short-term performance. Capri Holdings’ short-term incentive payouts rose well above the industry median since 2013. Due to the equity grants made to Mr. Idol during the most recently completed fiscal year, his pay spiked 1.2 times the median industry peer level, according to CGLytics’ multiple of median analysis.

As a result of these concerns, and following a qualitative assessment of the pay program, Glass Lewis recommended against supporting Capri Holdings’ executive compensation proposal for the 2019 annual meeting.

Conclusion:

Overall, the additional quantitative analysis using CGLytics underscored the concerns initially highlighted by Glass Lewis’ pay for performance grade by illustrating issues with pay regardless of the impact of Mr. Kors’ compensation on total NEO pay.